There is a question that should keep you up at night. What if the mainstream explanation for how currencies die is fundamentally flawed? What if the standard story confuses cause and effect, and the real mechanism has been hiding in plain sight for over a century?

Recent academic research dug into the actual historical records of the worst currency collapses of the 20th century. Not the usual statistics everyone cites, but the actual central bank balance sheets, internal government memos, bond prices, and archival documents from the 1920s. What came out of that research challenges almost everything the standard textbooks teach about severe inflation.

The implications reach far beyond history. They reach directly into the eurozone today.

The story everyone tells (and why it doesn’t add up)

Open any macroeconomics textbook and the explanation for hyperinflation reads like this: the government prints too much money, people rush to spend it before it loses value, prices explode, and eventually the currency becomes worthless internationally.

More money chasing the same amount of goods. Simple supply and demand. Case closed.

Except the data doesn’t support this story. Not even close.

When researchers lined up the actual weekly data from Weimar Germany, they found something that should have shattered this narrative decades ago. The money supply was growing only moderately for a long stretch after World War I. Yet the exchange rate collapsed dramatically. The thing that changed wasn’t how much money existed. It was what was backing that money.

Even more damning: after the German hyperinflation was stabilized in late 1923, the money supply increased fifteenfold. Prices stayed flat. The exchange rate held steady. If the textbook story were true, that should have been impossible.

Money on a leash

Here is the idea that changes everything.

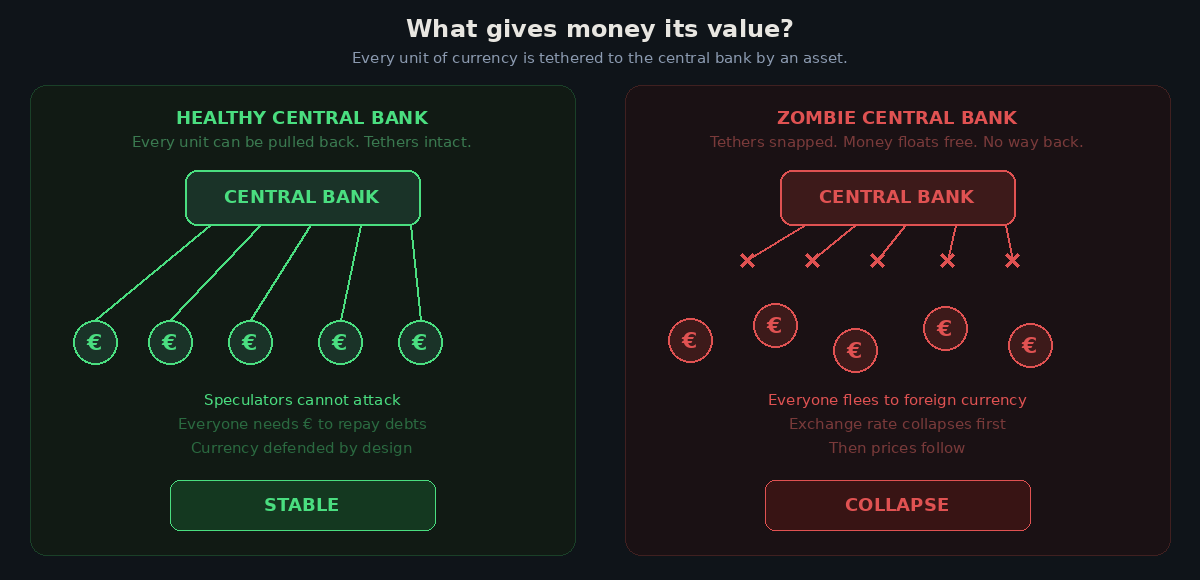

When a central bank creates money, it does not simply print it and scatter it into the economy. Every unit of currency enters circulation against a corresponding asset: a loan that must be repaid, a bond that will mature, a claim on something real. Economically speaking, every euro, every dollar, every peso is on an invisible leash. The central bank can always pull it back.

This is what gives money its value. Not just scarcity. Not just the fact that it is legal tender. But the fact that someone in the economy owes that money back to the central bank, and when they repay it, that money ceases to exist.

As long as every unit of currency has a thick, strong leash attached to it, the central bank is in control. It can absorb money back, defend the exchange rate, and maintain purchasing power. Speculators cannot successfully attack the currency because anyone betting against it will eventually need that currency to settle their own debts.

The moment those leashes snap, everything changes.

How currencies actually die

When a central bank loads its balance sheet with junk (worthless government IOUs, loans that will never be repaid, assets that exist only on paper), it loses the ability to pull money back. The leashes are gone. The currency is floating free.

Speculators notice first. They see the balance sheet deteriorating and start converting the domestic currency into dollars, pounds, or any other stable alternative. Then the broader public follows. Not because people want to buy more goods. They want to preserve their savings in something that still works as money. They run to the currency exchange, not to the supermarket.

This is exactly what you can observe in Argentina right now. Despite government restrictions, an entire parallel dollar economy thrives in the streets. The government tries to ban currency exchange, regulate exchange rates, punish violators. None of it works. The demand for stable money is too strong for any regulation to contain.

The exchange rate collapses first. Then domestic sellers adjust their prices upward to reflect the new reality. This is the exact opposite of the textbook story, where domestic prices rise first and the exchange rate follows.

Statistical tests on the 1920s data confirm this reversed causality. The correlation between exchange rates and prices is extremely strong. The correlation between the money supply and prices? Statistically not significant. The textbook relationship simply does not exist in the data.

The Chernobyl analogy

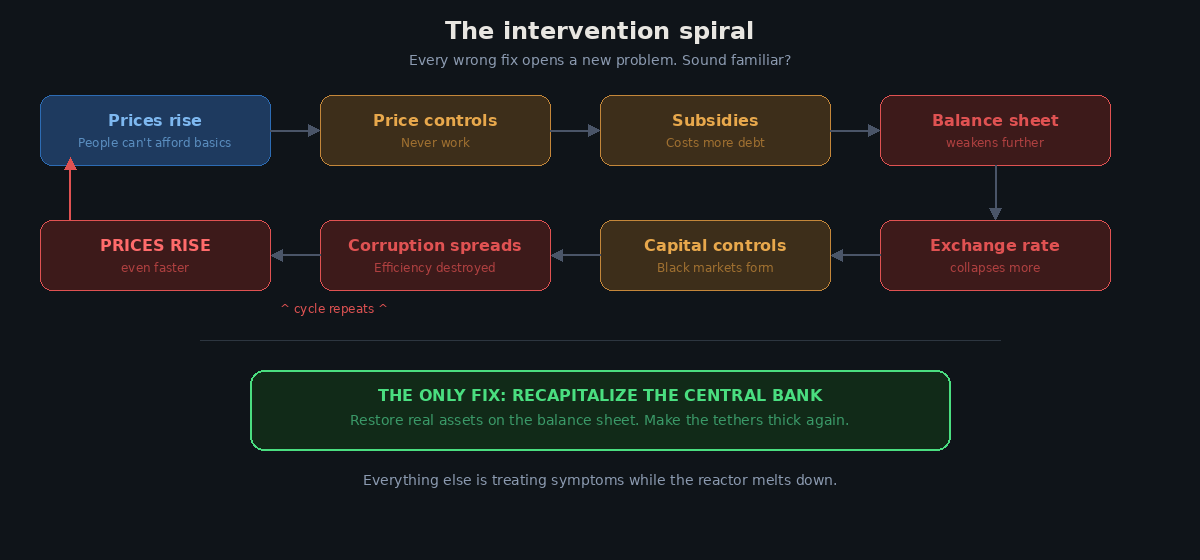

Think of it like the Chernobyl disaster. The reactor core is the central bank balance sheet. The Geiger counter is the exchange rate. When the Geiger counter goes haywire, you have two choices. You can try to fix the Geiger counter (regulate prices, ban currency exchange, impose capital controls). Or you can fix the reactor.

Every government facing severe inflation has tried option one first. Every single time, it has failed. And every time, the attempt created massive collateral damage.

Price controls lead to shortages. Subsidies require more government debt, which further weakens the central bank. Capital controls create black markets and corruption. The economy gradually drifts from free market allocation toward something that resembles central planning. Efficiency collapses. Real output falls. The population gets poorer in absolute terms, not just in monetary terms.

The only thing that has ever worked is fixing the reactor. Recapitalizing the central bank. Restoring real assets on the balance sheet. Making the leashes thick and strong again.

How they actually stopped it

The common myth about Germany is that a new currency replaced the old one and magically stopped the inflation. That is not what happened.

What actually happened was a recapitalization of the old central bank. The government imposed a special levy on all agricultural and industrial land. This created a stream of real, enforceable future payments. Those payments had present value. That value was transferred to the central bank’s balance sheet.

The old currency was then fixed to the dollar. Not the new one. The old one. With real assets backing it again, speculators could no longer attack the exchange rate because anyone who bet against the currency would eventually need it to repay their own debts. The speculation collapsed within weeks.

The formal currency reform came eight months later. By that point it was just cosmetic. Swapping out banknotes with twelve zeros for cleaner ones.

Every other hyperinflation of the era ended the same way. Recapitalize the central bank. Restore balance sheet quality. Stabilize the exchange rate. The money supply was irrelevant. In every case it kept growing substantially after stabilization, with zero inflationary effect, because the new money had strong leashes.

What this means for the eurozone

The eurozone is nowhere near hyperinflation territory. That needs to be stated clearly. The severity of today’s situation is not comparable to post-war Germany or modern Argentina.

But the pattern of errors is recognizable. And that should concern anyone paying attention.

Over the past fifteen years, the European Central Bank has progressively weakened its balance sheet quality. Before 2010, nearly all central bank money was issued against short-term, well-collateralized loans to commercial banks. Thick leashes. Since then, the system has shifted to three-year lending with weaker collateral standards, massive purchases of long-term government bonds from fiscally fragile member states, and a general loosening of the rules that kept the asset side robust.

The system’s equity position, valued at market prices rather than the book values officially reported, is hovering near zero.

Then there is the internal imbalance problem. Within the eurozone, national central banks have accumulated enormous claims against each other. If the euro were ever to break apart, there is no legal mechanism guaranteeing these claims would be settled. The country most people assume would be the big winner in any breakup would actually face the biggest hole in its central bank balance sheet. The resulting new currency would not be the rock-solid alternative everyone imagines.

Both sides are wrong

Here is the uncomfortable punchline.

The optimists who say the central bank can solve every problem by buying more bonds and extending more credit are making things worse. Every such action weakens the balance sheet and moves closer to the danger zone.

The critics who warned for years that the massive growth in money supply would cause inflation were watching the wrong indicator. When inflation didn’t materialize, their credibility suffered. But they were right that something dangerous was building. They were just wrong about what. It wasn’t the quantity of money that mattered. It was the quality of what was backing it.

Both camps missed the central bank balance sheet. The actual variable that determines whether a currency lives or dies.

The good news

Every historical case shows that the problem is solvable. Even in the absolute worst conditions, with an occupied industrial heartland and zero foreign credit, countries have managed to stabilize. The formula is clear: restore balance sheet quality, enforce strict collateral requirements, ensure fiscal discipline.

In today’s eurozone, this would be far easier than anything the 1920s generation had to deal with. Gradual return to shorter lending terms. Honest mark-to-market accounting. A credible plan for reducing sovereign bond exposure. Some fiscal adjustment. It would involve real but manageable pain.

The danger is not that Europe faces some impossible structural challenge. The danger is that the wrong diagnosis leads to the wrong treatment. And by the time enough people understand the actual mechanism, the fix has become far more expensive than it needed to be.

History is generous with second chances. But only for those paying attention.